How to Pass Your Wealth on to the Next Generation in the Most Tax Efficient Way

Rising property prices and significant inflation have, in real terms, lowered the Inheritance Tax (IHT) threshold with each passing year, resulting in more and more people finding themselves liable for IHT

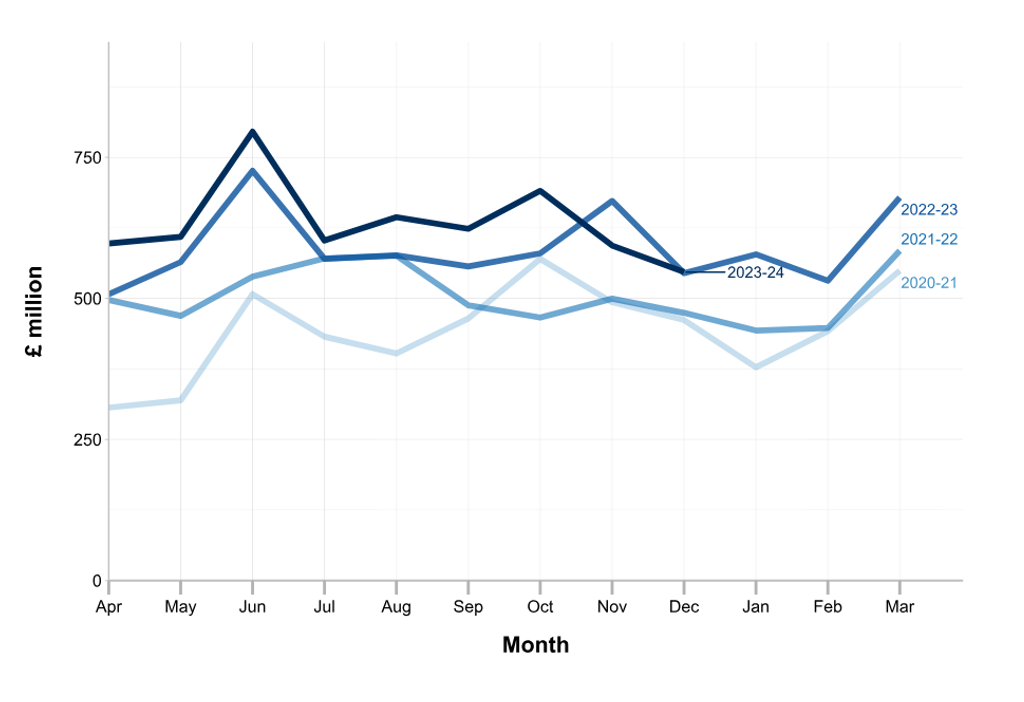

Between April 2023 and December 2023, HMRC receipts from inheritance tax (IHT) totalled £5.7 billion. This represents an 8% year on year increase, which in no small part is due to the fact that the IHT threshold has remained fixed since 2009/10. Effectively, fixing the IHT ‘nil-rate band’ in this way has meant that soaring property prices and inflation have, in real terms, lowered the threshold each year, meaning that many more people are now finding themselves caught in the IHT 'trap'.

Inheritance Tax (IHT)

IHT receipts for April 2023 to December 2023 were £5.7 billion, which is £0.4 billion higher than the same period a year earlier.

Monthly receipts

Source Gov.uk national statistics: HMRC tax receipts for the UK (monthly bulletin) published 23 January 2024

Inheritance Tax (IHT) in the United Kingdom (UK) is a tax on estates of individuals who have passed away. It is applicable to the assets left behind, including property, savings, investments, and personal belongings. For British expatriates, understanding the rules and regulations of IHT can be a complex process.

Estate Threshold

The first £325,000 of a UK domiciled individual’s estate is exempt from IHT. This is referred to as the ‘nil-rate band’ and is the amount an individual can leave to their beneficiaries without incurring an IHT liability. This figure increases to £500,000 if you own your home and pass your estate onto your children. If you share your estate with your partner or spouse, together you can pass up to £1 million onto your children before IHT is due. However, if your estate is worth £2 million or more, before allowing exemptions and reliefs, you will lose £1 of the main residence relief allowance for every £2 of value above £2m. So, for a couple with estates worth £2,350,000 or more, there will no main residence relief at all.

For UK expats, the domicile status of an individual plays a crucial role in determining their IHT liability. If the individual is UK domiciled but not resident in the UK, they will still be liable to IHT. If they are non-domiciled but have UK assets, the UK assets will be liable to IHT.

An individual would have to give up their UK domicile status to ensure no UK IHT liability on their assets abroad (i.e. giving up their UK passport, closing all UK accounts, severing all UK links etc). It can be incredibly difficult for UK nationals to change or lose a domicile and acquire a new ‘domicile of choice’. All ties to the UK must be cut, and these ties can be as basic as a bank account, golf club membership or even a library card, and a commitment to remain a long-term/permanent resident abroad must be evidenced.

The hard work done to acquire a new domicile can also be undone very quickly. For example, by moving to a third country, losing the acquired ‘domicile of choice’ will lead to your domicile status reverting to your initial ‘domicile of origin’.

Many of our clients whose ‘domicile of origin’ is not the UK, have left the UK with no intention of returning and are surprised to learn that their UK domicile has been retained. For inheritance tax purposes, this ‘deemed domicile’ acquired by living in Britain for a period, will continue for an additional three years beyond the date at which you acquire a new domicile of choice. During the ‘deemed domicile’ period it is important to seek advice on any tax planning steps so as not to fall foul of any unintended UK taxes whilst still deemed UK domicile. Finally, if you decide to be buried in the UK, this will also trigger UK inheritance tax.

In a previous article, we explained the various types of domicile in more detail, and I would recommend this piece to anyone who has changed their country of residence or is considering a move abroad at any stage in their life.

Even after going through the process of gaining a new domicile, it’s important to remember that any UK-based assets will still be liable to UK inheritance tax.

So if the value of your UK assets is likely to be in excess of the nil rate band threshold, how can you pass money down to the next generation in the most tax efficient way possible, without your beneficiaries having to pay an unnecessarily high IHT bill on their inheritance?

Trusts

The Government’s nil-rate band has remained frozen at £325,000 since the 2009/2010 tax year and it is set to stay the same until 2028. As mentioned, the additional £175,000 residence nil-rate band can provide some additional relief to UK homeowners with children, but with property prices having risen dramatically, even those who bought their homes for a modest sum may now be subject to IHT.

Setting up a trust can be an effective way to mitigate IHT, as assets held in trust are typically outside of an individual’s estate. This means that the assets in the trust are not subject to IHT when the individual dies.

There are a number of trusts that can be used as part of your estate planning, but to identify the structure that would work best for you and for your beneficiaries, one of our qualified advisors can discuss your specific circumstances and aims as part of an initial consultation.

Gift Rules

The UK operates a seven-year gift rule, which states that if an individual gives away an asset more than seven years before they pass away, it will be exempt from IHT. This can be one of the most effective ways to mitigate IHT, as making gifts during your lifetime can reduce the value of your estate and potentially reduce your IHT liability. However, if an individual gives away an asset within seven years of their death, the value of the asset will be included in their estate for IHT purposes.

If the individual were to pass away within 7 years of giving a gift, inheritance tax would be paid on a reducing scale. Gifts given up to 3 years prior to death are taxed at 40%, and gifts given between 3 and 7 years prior to death are taxed on a sliding scale known as ‘taper relief’.

The following gifts can be given in the 7 years prior to death without any IHT needing to be paid:

- Each year you can give up to £3,000 to anyone you like. You can also use the previous year’s exemption if you didn’t make use of it at the time. If, for example, your granddaughter was buying her first home, you and your spouse could potentially give her £12,000 for her deposit at once – assuming neither of you gave £3,000 away the previous year.

- If you have extra income that you don’t require, you can make regular gifts to others. It’s important that you keep a record of these.

- You can give your children up to £5,000 for their wedding and up to £2,500 to your grandchildren. Few people realise they can also give wedding gifts of up to £1,000 to others.

- Any donations made to charities or political parties are inheritance tax free, whether you give them in your lifetime or your will. This includes property, shares and land.

- You can reduce the rate of IHT for your whole estate to 36% by leaving at least 10% of your net estate to charity in your will.

Family Investment Company

Sometimes outright gifts to family members might not be appropriate. However, holding investments in a separate company – a ‘Family Investment Company’ (FIC) – might be a good alternative option.

An FIC enables you to benefit from lower tax rates on investment income and gains. The timing of tax liabilities on the distribution of funds to shareholders can also be managed.

To find out more about setting up a Family Investment Company and whether this could be the right option for you and your family, speak with one of our qualified advisors who will be glad to discuss this with you as part of an initial consultation.

Creating and reviewing a will

Creating and regularly reviewing and updating your will can help to ensure that your assets are distributed in the most tax-efficient manner. You should consider writing a will that takes advantage of the nil-rate band and other reliefs and exemptions available to reduce your IHT liability. We can explain this in more detail and put you in touch with someone who can arrange this for you.

Preparation, planning and protecting your estate

And it’s important to remember that UK tax laws and regulations can be complex and may change over time, so it’s important that you seek professional advice from a qualified advisor and ensure that you continue to take the most efficient steps to protect your estate and mitigate your IHT liability.

To speak with one of our expert advisors about your estate and inheritance tax planning and how we can help you pass on your wealth to your loved ones in the most tax efficient way possible, contact us today - and to download our Guide to Estate and Inheritance Tax Planning click here.

Read more of our latest articles

Please complete the form below with your details and we will get back to you as soon as possible.