2025 Wealth Migration: Why a Record 16,500 Millionaires Are Leaving the UK - And Where They're Going

Why the UK is Facing a Historic Wealth Drain in 2025

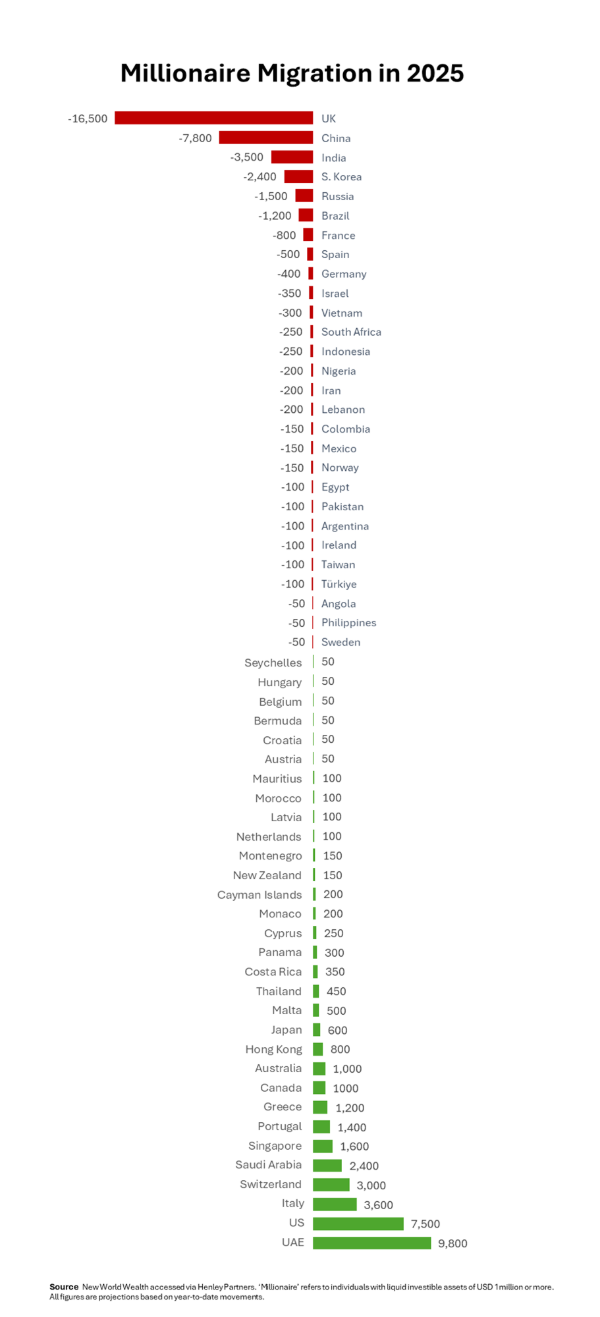

In 2025, the UK is projected to lose a record 16,500 high-net-worth individuals (HNWIs), according to the latest Henley Private Wealth Migration Report.

This exodus of HNWIs from the UK marks the steepest net outflow of millionaires

ever recorded for any country - more than double the number expected to leave China.

This mass movement of wealth is driven by a confluence of new tax regulations, changing residency rules, and evolving geopolitical dynamics.

What’s Changed Since 2024?

In 2024, approximately 7,500 millionaires left the UK, a figure that was already cause for concern among UK policymakers. However, in 2025, this number has more than doubled to a record 16,500, marking the steepest annual increase of HNWI net outflows on record.

This unprecedented spike has been driven by the formal enactment of the non-domicile (commonly known as ‘non-dom’) abolition and inheritance tax reforms introduced in April 2025, alongside the tax hikes implemented in October 2024.

While 2024 saw the groundwork being laid, 2025 has seen the full effect of these reforms take hold, prompting a dramatic acceleration in relocation planning among wealthy individuals.

What’s Causing the Surge in Millionaire Migration

1. Abolition of Non-Dom Status

In March 2024, the UK government formally abolished the long-standing non-domicile regime. This significant policy shift removed long-standing tax exemptions for foreign income and gains, fundamentally altering the tax landscape for wealthy individuals with international assets or income streams.

2. Tax Hikes and Complexity

Commencing in October 2024, the UK implemented considerable increases to key tax categories, including Capital Gains Tax (CGT), Inheritance Tax (IHT), and corporate tax. These developments have increased both the cost and complexity of maintaining personal and business wealth within the UK, particularly for affluent families and investors.

3. Loss of Investor-Friendly Visa Options

The UK’s decision to discontinue the Tier 1 Investor Visa, paired with the broader tightening of immigration frameworks, has significantly reduced the appeal of the UK as a destination for internationally mobile entrepreneurs and HNWIs seeking residency through investment.

4. Political and Economic Uncertainty

A climate of ongoing fiscal uncertainty; with further tax hikes and the potential implementation of a ‘wealth tax’ in the forthcoming Budget announcement widely anticipated; rising inflationary pressures; and growing concern over the UK’s long-term economic competitiveness; has contributed to a general sense of instability among the wealthy. These factors are prompting many to seek more predictable and business-friendly jurisdictions abroad.

Where Are UK Millionaires Moving To?

High-Net-Worth individuals are not simply fleeing the UK; they are seeking environments that support long-term growth, privacy, and efficient wealth structuring. Here’s a deeper look at the top destinations and what makes them attractive:

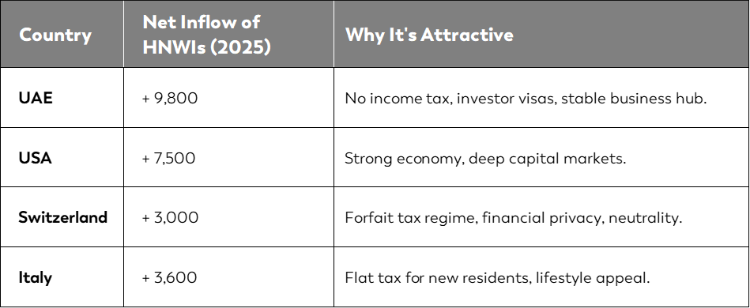

United Arab Emirates (UAE)

The UAE continues to dominate wealth migration tables for its combination of zero personal income tax, world-class infrastructure, and globally respected residency schemes. Dubai in particular offers high-end real estate, international schools, and Golden Visa options for long-term stability.

Switzerland

Switzerland remains a top choice due to its political neutrality, stable economy, and privacy-oriented financial system. The forfait (lump-sum) taxation system allows qualifying Ultra High Net Worth (UHNW) foreign nationals to negotiate fixed annual tax payments, irrespective of actual income or wealth. Download our Financial Guide to Switzerland for Expats.

United States

The US remains an attractive destination for both HNWIs and UHNWIs, particularly tax-friendly states like Florida and Texas. Both states offer no state income tax, making them attractive for HNWIs and UHNWIs seeking to mitigate tax exposure. In addition, the US provides significant business and investment opportunities, particularly in technology, real estate, and financial markets.

For UHNWIs, cities like Miami and Houston have become epicentres of luxury real estate, with a growing international presence. The country’s reputation for innovation and entrepreneurship further adds to its appeal for individuals looking to grow their wealth. Download our Financial Guide to the United States for Expats.

Italy

Italy’s flat tax regime offers new residents the ability to cap foreign income tax at €100,000 per year for up to 15 years. This, combined with lifestyle advantages and growing international hubs like Milan, is attracting HNWIs from the UK and beyond.

What Does This Mean for UK-Based Wealth?

The projected outflow of approximately £66 billion in liquid assets from the UK in 2025 represents a substantial shift in private capital, with wide-ranging economic implications. These include potential cooling in the UK property market, reduced participation in private equity and domestic investment funds, diminished tax revenues, and possible constraints on the funding of public services. Over time, these effects could also weigh on the UK's long-term economic growth and competitiveness.

At the individual level, this trend underscores the importance of reviewing key aspects of one’s financial strategy. This includes potentially re-evaluating residency status, considering more tax-efficient asset structures, and planning for wealth succession, particularly in light of the inheritance tax reforms introduced in April 2025. These changes are expected to begin influencing tax exposure during the 2025/26 tax year, depending on an individual’s UK residence history.

Strategic Financial Planning Consideration

With the UK having shifted to a residency-based inheritance tax system as of 6 April 2025, your liability is now determined by whether you have been UK-resident for at least 10 of the past 20 tax years. These recent changes require careful consideration when managing international wealth. Here are four key strategic planning considerations:

- Explore Residency Options: Establishing Non Long Term UK Residence could help reduce future UK inheritance tax exposure and support your broader financial objectives.

- Structure Your Assets Internationally: Reducing your UK situs assets, and using tax wrappers such as offshore bonds, as well as trusts and corporate structures, may offer greater flexibility and potential tax efficiencies.

- Plan Succession Carefully: Ensure that your wills and estate plans are compliant in both the UK and the countries where you hold assets and/or are resident, to avoid unintended tax consequences.

- Mitigate Currency Exposure: Holding assets in currencies aligned with your future spending needs can help mitigate currency risk over time.

Making the Complex Simple for British Expats Worldwide

At Forth Capital, we specialise in helping high-net-worth (HNW) internationally mobile executives build, optimise, and protect their wealth - before, during and after a move abroad. From optimising your tax position and managing currency exposure, to asset management and estate planning, we provide clear, transparent, personalised advice to help you ensure that your wealth is structured tax-efficiently and that costly mistakes are avoided.

We work closely with clients facing global financial challenges, offering joined-up solutions that align your investments and assets with your long-term goals. The aim is simple: effective, integrated planning that works wherever life takes you.

If you’d like to schedule an initial consultation with me to discuss your financial planning, wealth management or pensions please

get in touch today.

Jamie Tulip DipFA PETR

Chartered International Financial Planner

As a dual-qualified and dual-licenced Chartered Financial Planner, I offer tailored financial planning services to international private clients. I help them understand their options, optimise their cross-border pensions and investments, and create a robust financial plan for their future lives.

Frequently Asked Questions

The departure of HNWIs from the UK is primarily driven by a combination of new tax policies, including the removal of non-domicile status, changes to Capital Gains Tax (CGT) and Inheritance Tax (IHT), and a perception that the UK is becoming a less favourable environment for wealth preservation and growth.

Popular destinations include the UAE, USA, Switzerland, Italy, Portugal, Greece, and Saudi Arabia. These countries offer favourable tax treatment, investor visa routes, and potentially, greater fiscal stability.

From 6 April 2025, the UK replaced its domicile-based inheritance tax system with one based on long-term residence. If you have been non-UK resident for at least 10 of the previous 20 tax years, your non-UK assets may fall outside the scope of UK IHT. This change could potentially benefit expatriates and globally mobile individuals.

Yes. While the UK's new tax framework may reduce some of the previous planning flexibility, strategies remain available to help mitigate exposure. These include tax-efficient investment wrappers, and careful succession planning. Early, tailored planning remains essential.

It is important to begin with a thorough review of your tax residency status, estate planning, and the structure of your global assets. An international Financial Planner may be able to assist you in identifying jurisdictions and strategies that best support your long-term financial goals, reduce tax risk, and ensure compliance across multiple countries.

¹The Henley Private Wealth Migration Report 2025

This communication is for information purposes only and does not constitute financial, legal, or tax advice. All content is based on current UK legislation and is subject to change. All planning arrangements should be regularly reviewed in consideration of legislative updates. Pension regulation and tax treatment vary between jurisdictions. Any reference to UK or international pension rules is portrayed in general terms and is not intended to reflect individual circumstances. Any examples provided are hypothetical and for illustrative purpose only. Outcomes will differ based on individual circumstances and local law and regulation. Pension transfers carry specific risks and may not be appropriate for everyone. The suitability of any transfers or investments should be assessed on an individual basis. Past performance is not a reliable indicator of future results. The value of investments can fall and rise, and you may not get back the amount originally invested.

Last updated 24 July 2025

Read more of our latest articles

Worldwide

Licences